European banks rally, Iron ore falls 8%, RBA minutes, Graincorp, BHP, Zip Co on watch: ASX to rise

Wall St is closed for the Juneteenth holiday. Europe rebounded as dip buyers emerged, helped by banks and energy.

Good morning. I’m Melissa Darmawan for Finance News. This is your market outlook.

The Australian sharemarket, set to rebound amid US futures for the Dow, S&P 500 and Nasdaq up 1 per cent each.

European banks, travel, leisure stocks rally

Wall St is closed for the Juneteenth holiday, a commemoration of the end of slavery after the American civil war. We will look to the European markets for our lead today.

The Stoxx 600 rose almost 1 per cent after last week’s sharp sell-off. Investors reacted to ECB president Christine Lagarde's statement that the risk of a steep correction in Europe’s financial assets and housing prices remains “severe”. Ms Lagarde also reaffirmed plans to increase Eurozone interest rates twice in the coming months.

At the closing bell, Paris added 0.6 per cent amid President Macron's party losing an absolute majority in the country’s parliamentary election. Frankfurt gained 1.1 per cent, while London’s FTSE added 1.5 per cent, thanks to a lift in BP, it rose 3.2 per cent and Shell added 3.3 per cent. Rio bucked the trend, closing 1 per cent lower.

Banks, travel, leisure and energy companies led the advance in the Stoxx Europe 600 index by 3.3 per cent, 3 per cent, and 2.1 per cent respectively. Basic resources added 0.7 per cent amid a slump in raw-material prices, while construction companies were the worst performer, down 1.8 per cent.

Let’s take a look at what this means for the Aussie market today.

Figures around the globe

Asian markets closed mixed, Tokyo’s Nikkei lost 0.7 per cent, Hong Kong’s Hang Seng added 0.4 per cent while China’s Shanghai Composite closed flat, down 0.04 per cent..

Yesterday, the Australian sharemarket fell 0.6 per cent to 6,433.

SPI futures

Taking all of this into the equation, the SPI futures are pointing to 0.7 per cent gain.

What to look out for today

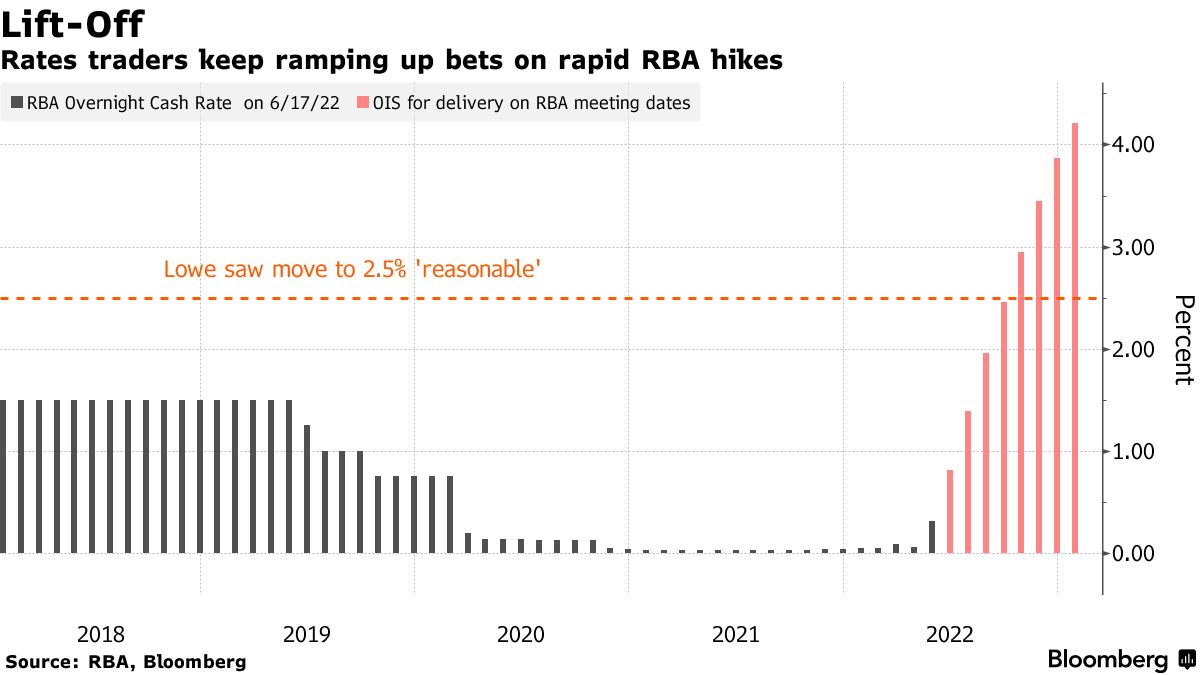

The RBA meeting minutes are due today, following figures indicating a tight labour market and rising inflation expectations. The weekly consumer confidence figures from ANZ and Roy Morgan are due.

To recap, the economy created 60,600 jobs and the unemployment rate remained unchanged at 3.9 per cent. While inflation expectations grew sharply to 6.7 per cent in June, from 5.0 per cent in May.

Ahead of the minutes due at 11.30am AEST, investors will also hear from governor Philip Lowe when he gives a speech called “Inflation and Monetary Policy.” Mr Lowe said last week that the RBA would do “what’s necessary” to bring inflation down to the 2 to 3 per cent target and that it’s “reasonable” to expect the policy rate will rise to 2.5 per cent from 0.85 per cent now.

Money market traders see an increasing likelihood of the RBA, following the Federal Reserve with a 75-basis-point interest rate hike in July or August. Overnight index swaps have priced in a 50 per cent chance of this move in the coming two months, as pricing ramps up ahead of the minutes today.

Even with the super-size hike, the RBA is playing catch-up. Investors will be combing through the meetings for any signs from the central bank on its plans to raise interest rates by 50 basis points. This will bode well for the Australian dollar against the greenback which has fallen over 1.6 per cent last week.

In outlook, Graincorp (ASX:GNC) has their investor day scheduled today while in M&As, there is speculation that Adbri (ASX:ABC) has put in an offer to buy Western Australian building products business BGC Group, according to the AFR.

Miners Vale SA and BHP (ASX:BHP) said that they’re not interested in selling their joint venture Samarco after reports of the interest of Brazilian steelmaker Companhia Siderurgica Nacional.

"BHP Brasil and Vale say Samarco is not for sale and reaffirm its support for the restructuring plan filed by the employees' unions," the companies said in a joint statement.

Zip Co’s (ASX:ZIP) business in the UK is under heavy scrutiny from the directors, with suggestions the board has appointed a consultant to consider options for that part of the business, according to The Australian.

Lastly, Premier Investments ASX:PMV) is trading ex-dividend today, which means the share price is likely to trade lower. Eligible shareholders are set to receive 46 cents per share of the fully franked dividend on 27 July.

Ex-dividend

There are two companies set to trade without the right to its dividend.

Kelly Partners Group Holdings (ASX:KPG) is paying 0.363 cents fully franked

Premier Investments (ASX:PMV) is paying 46 cents fully franked

Dividend-pay

There are four companies set to pay eligible shareholders today

Coronado Global Resources (ASX:CRN)

Fat Prophets Global Contrarian Fund (ASX:FPC)

Oceania Healthcare (ASX:OCA)

Virgin Money Uk Plc (ASX:VUK)

Commodities

Iron ore has lost 8 per cent to US$112.35. Its futures point to a 3.1 per cent fall.

Gold has added $0.10 or 0.01 per cent to US$1840.70 an ounce. Silver was down $0.02 or 0.07 per cent to US$21.67 an ounce.

Oil has added $0.71 or 0.7 per cent to US$110.27 a barrel.

Currencies

One Australian Dollar at 7:10 AM has strengthened since yesterday, buying 69.55 US cents (Mon: 69.30 US cents), 56.77 Pence Sterling, 93.93 Yen and 66.17 Euro cents.

Disclaimer

The content is for educational purposes only and does not constitute financial advice. Independent advice should be obtained from an Australian Financial Services Licensee before making investment decisions. To the extent permitted by law, SEQ excludes all liability for any loss or damage arising in any way including by way of negligence.

Sources: Bloomberg, FactSet, IRESS, TradingView, UBS, Bourse Data, Trading Economics

Copyright 2022 – Finance News Network

Source: Finance News Network